The September jobs report brought a surprising wave of optimism, with the U.S. economy adding a net gain of 254,000 jobs, surpassing expectations.

This sharp increase in employment numbers initially sparked discussions about the potential for a “soft landing” as market participants looked for signs that the economy could escape a recession.

While the unemployment rate saw a slight decline from 4.2% to 4.1%, questions remain about whether this growth is sustainable in the long term, particularly as the Federal Reserve navigates the complex dynamics of monetary policy.

Interest Rates Cuts Expected to Slow

The robust job growth paints a positive picture, marking the largest monthly increase since March. For some, this data suggests that the Federal Reserve might be able to slow the pace of its aggressive interest rate cuts, which have dominated the year so far.

With expectations shifting, the market now leans towards more modest quarter-point reductions in November and December, as opposed to the earlier, larger cuts. Traders are becoming more cautious, tempering their outlook with the realisation that economic conditions could change.

Yet, the skepticism surrounding this report is hard to ignore. While the headline numbers indicate strength, the bulk of the job gains occurred in sectors such as food services, healthcare, and government.

These areas have been propped up by fiscal stimulus, casting doubt on whether the gains represent broader economic resilience.

Manufacturing and Technology Slow to Grow

More concerning for the Federal Reserve is the slower growth in manufacturing and technology, sectors that are key to the economy’s overall health. These weaknesses may explain why the Fed continues to pursue rate cuts, despite what seems like a thriving labor market.

Moreover, labour market data tends to be a lagging indicator, reflecting conditions that may no longer be relevant. The strong job numbers could be pointing to past economic strength rather than future prospects.

Reconciling Job Growth with Economic Risks

In contrast, the Federal Reserve often bases its decisions on forward-looking data, including inflation expectations, consumer spending, and global economic factors. This leaves the central bank with a dilemma: how to reconcile the upbeat job data with the broader signs of economic fragility that persist in other sectors.

As we move forward, the Federal Reserve’s decisions will be closely watched. While the labor market appears strong for now, the uneven distribution of growth across sectors and the lagging nature of employment data suggest that caution is warranted.

Technical Analysis for the Week

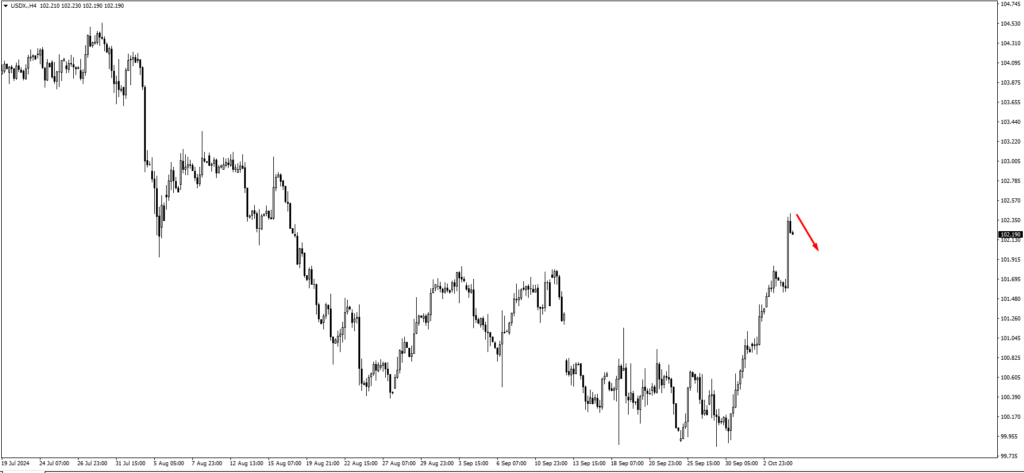

The technical landscape is similarly complex. We observed that the US Dollar Index (USDX) ended the week around 102.40, a level closely monitored after the release of the Non-Farm Payroll report.

This position has now set the stage for two potential short-term scenarios: a downward move that could break the support at 99.86, or a period of consolidation before an eventual decline.

For traders, the next few sessions will be essential to watch as the price action in this zone will either confirm a new low or signal a temporary upward correction.

EURUSD Trend

In the EURUSD pair, which has been trading near the 1.0940 area, two possible outcomes are also in play. If EURUSD pushes higher from this level, it may break through the 1.12134 swing high, which would indicate strength in the euro.

However, if the price consolidates at the current level, the currency pair could decline in the short term before resuming its upward trajectory. Traders will need to be vigilant about how the euro behaves in this zone, as it could signal the start of a new trend.

USDJPY Trend

The USDJPY pair has reached 148.90, and the possibility of a downturn is high, especially with concerns about inflation in Japan.

A test of the 150.00 level could occur, but traders should watch for bearish price action in this area. How the pair behaves around this psychological threshold will play a pivotal role in setting the short-term trend, with any signs of weakening yen likely to push USDJPY lower.

AUDUSD Trend

For AUDUSD, which is trading around 0.6770, there’s a chance it could test this level more thoroughly before moving higher. Alternatively, if the price drops lower, traders should focus on 0.6710, a zone that could attract buyers.

In either case, watching for bullish price action in these areas will provide insight into the strength of the Australian dollar as it navigates current market pressures.

Technical Trends for Commodities and Gold

In commodities, US Oil has been on an upward trajectory, breaking the 73.25 mark amid heightened tensions between Israel and Iran.

If price consolidates, traders should look for bullish action around 72.05, as the potential for further conflict could fuel upward momentum. Any breakout in war would likely push oil prices even higher, making this a highly volatile market to watch.

Gold Continues Climbing

Gold, which has traded higher from the 2640 area, faces resistance around 2760. If the price fails to break this level, traders should look to 2590 as the next possible target.

Both levels provide critical zones for gold, where price action will determine whether the precious metal continues its upward trend or pulls back to test lower levels.

The SP500 also saw upward movement, but it did not reach the monitored 5650 level before its rise. We could see the index test the 5900 mark next, where traders will be keen to observe how the market reacts at these lofty heights.

The resilience of the SP500 amidst these macroeconomic developments remains in focus.

Key Events this Week

This week, the markets will see several economic reports and central bank decisions, all of which will likely impact the markets.

Starting on Wednesday, the market will first focus on New Zealand’s official cash rate decision, which is forecasted to drop to 4.75% from the previous 5.25%.

If the rate cut occurs, it will highlight the Reserve Bank of New Zealand’s ongoing concerns about the strength of its economy, particularly in the face of global headwinds.

A lower interest rate could weaken the New Zealand dollar, prompting traders to consider selling NZDUSD early in the week, especially if the pair tests the 0.6160 area again. A sustained drop could see the kiwi testing even lower levels like 0.6080.

U.S. Inflation Data Release

As we move into Thursday, all eyes will turn to the U.S. inflation data, with core CPI forecasted to come in at 0.2% month-over-month, compared to the previous reading of 0.3%. The year-over-year inflation rate is expected to slow to 2.3% from 2.5%, indicating that the Federal Reserve’s aggressive tightening might finally be having its intended effect.

If inflation cools as predicted, it would give the Fed more flexibility in its approach to interest rate cuts for the remainder of the year.

However, if inflation surprises to the upside, the U.S. dollar could strengthen sharply, potentially causing a drop in pairs like EURUSD and GBPUSD, which are currently sitting at pivotal levels.

U.K. Monthly GDP Report and U.S. PPI Release

On Friday, the U.K. will release its monthly GDP report, with expectations set at a 0.2% increase after a flat reading in the previous month. This positive forecast signals mild economic growth, though traders remain wary of any unexpected economic slowdown.

The British pound could see upward momentum if the GDP data meets or exceeds expectations. However, consolidation in the currency pair could signal that traders are cautious, especially with a weaker U.S. dollar potentially driving GBPUSD higher.

The U.S. producer price index (PPI) report is also due, and the forecast for a 0.1% increase month-over-month suggests that inflation pressures in the supply chain might be easing.

If the PPI comes in higher than expected, it would reinforce concerns about sticky inflation, further influencing the Fed’s approach to monetary policy and potentially boosting the U.S. dollar.

In contrast, a softer PPI reading would align with the expectation of lower inflation, providing some relief for the Fed as it weighs future rate cuts.